Most people when they think of refinancing their home mortgage just pick up the phone and call around or answer an advertisement. In the long run they may be missing an opportunity to further their long-term financial goals by taking a different approach.

Your home is typically your most important investment and any loan on that home will have a long-term effect upon your finances. We advocate not only working with an experienced lender, but working with a team to make sure that your options are selected in a way that will help you today and many years from now.

Who should be part of your team? In addition to an experienced and knowledgeable lender, your team should also include your financial advisor. It is your advisor who should know where your goals lie. A tax advisor also might be part of this team because your home is likely also to represent your most important tax deduction.

Even the simplest of decisions may need the help of your advisor team. Say that interest rates have decreased and you are looking to lower your payment. Even in this case there may be several options…

• Opt for the lowest rate and pay closing costs out-of-pocket.

• Opt for the lowest rate but increase your loan amount to pay for closing costs.

• Opt for a slightly higher rate which will give you a lender credit to pay for closing costs.

What variables would affect the right decision in this regard? Your cash reserves, how long you expect to have the mortgage, your equity position and more. And the options do not end here. There may be other objectives you can achieve by obtaining a lower rate.

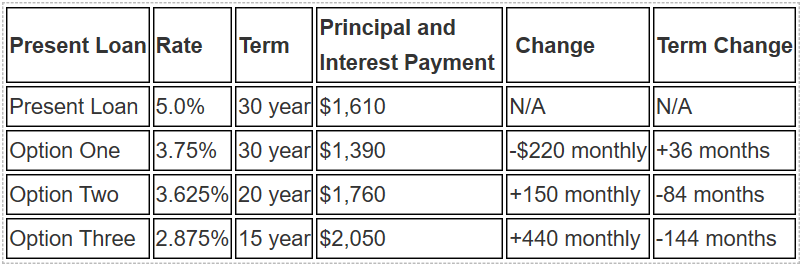

What if one could use a lower rate to shorten the term of their mortgage? Ordinarily, refinancing will increase the term of a mortgage. For example, if a homeowner obtained a 30 year loan three years ago and refinanced today, they would be increasing the term from 27 years to 30 years. However, if they are lowering the rate, they could also opt to decrease the term at the same time. Let’s take a hypothetical example. Note that all rates and payments in this example are for example purposes only and are approximate. In addition, the issue of closing costs for each option are not addressed.

$300,000 Present Mortgage

5.0% Rate

Principal and Interest Payments of $1,610

Let’s say rates have dropped and the homeowner has the three hypothetical options. The following chart demonstrates these in terms of payment reduction or increase as well as term reduction or increase—

Which is the best alternative in this situation? It depends upon the financial situation of the homeowner and that is why a financial advisor is an important ingredient within the process. The answer for someone who is 30 years old and someone who is 50 years old could be completely different. Variations in income levels, cash reserves, retirement objectives and more would all be a consideration.